For years, the Merchant Cash Advance (MCA) has been marketed as a “quick fix” for cash-strapped businesses. But in 2026, the data shows a different story: a surge in corporate bankruptcies fueled by “Mob Math” and debt stacking.

The “Bite” You Don’t Feel (Until It’s Too Late)

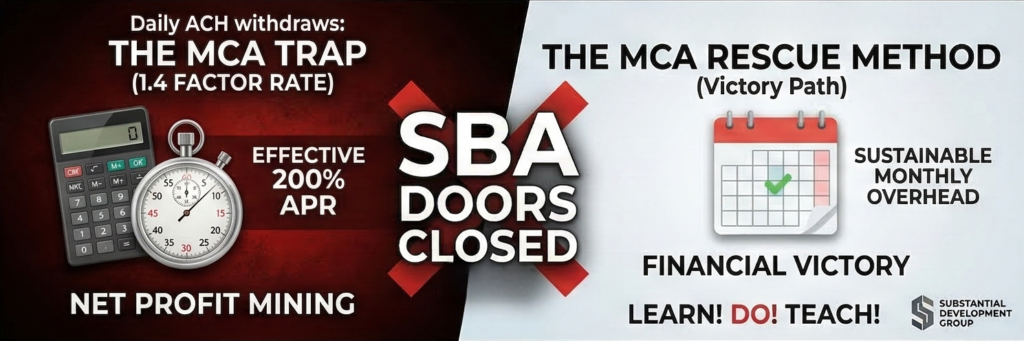

Business owners often normalize the daily ACH withdrawal because it feels manageable at first. However, a factor rate of 1.4—which sounds like a 4% fee—is actually closer to a 200% APR when you account for the daily repayment schedule. You are essentially working for the funder while they take the lion’s share of your net profit.

The SBA Door is Closed

Historically, many owners planned to “bridge” their way through high-cost funding until they could qualify for a traditional SBA 7(a) loan. That strategy is officially dead. As of June 1, 2025, SBA rules prohibit using loan proceeds to refinance MCA or factoring arrangements. To be clear: while factoring is the sale of an asset and not “debt” in the traditional sense, the SBA now classifies it as an ineligible obligation for refinancing. If you are utilizing these tools today, you cannot look to the SBA to pay them off later.

The Victory Path: The MCA Rescue Method

We guide you to overcome this trap through a principled three-step approach:

- Learn: Identify the “True Lender” violations in your contract.

- DO: Implement structured protection to stop the daily drain without triggering a total collapse.

- Teach: Master your cash flow so you never have to rely on predatory capital again.

The Bloomberg data is clear: stacking is a precursor to collapse. Don’t be the next statistic.